This page serves as a public archive and technical reference documenting how the El Dorado Hills Community Services District (EDHCSD) forensic audit was deliberately orchestrated, manipulated, and limited in scope.

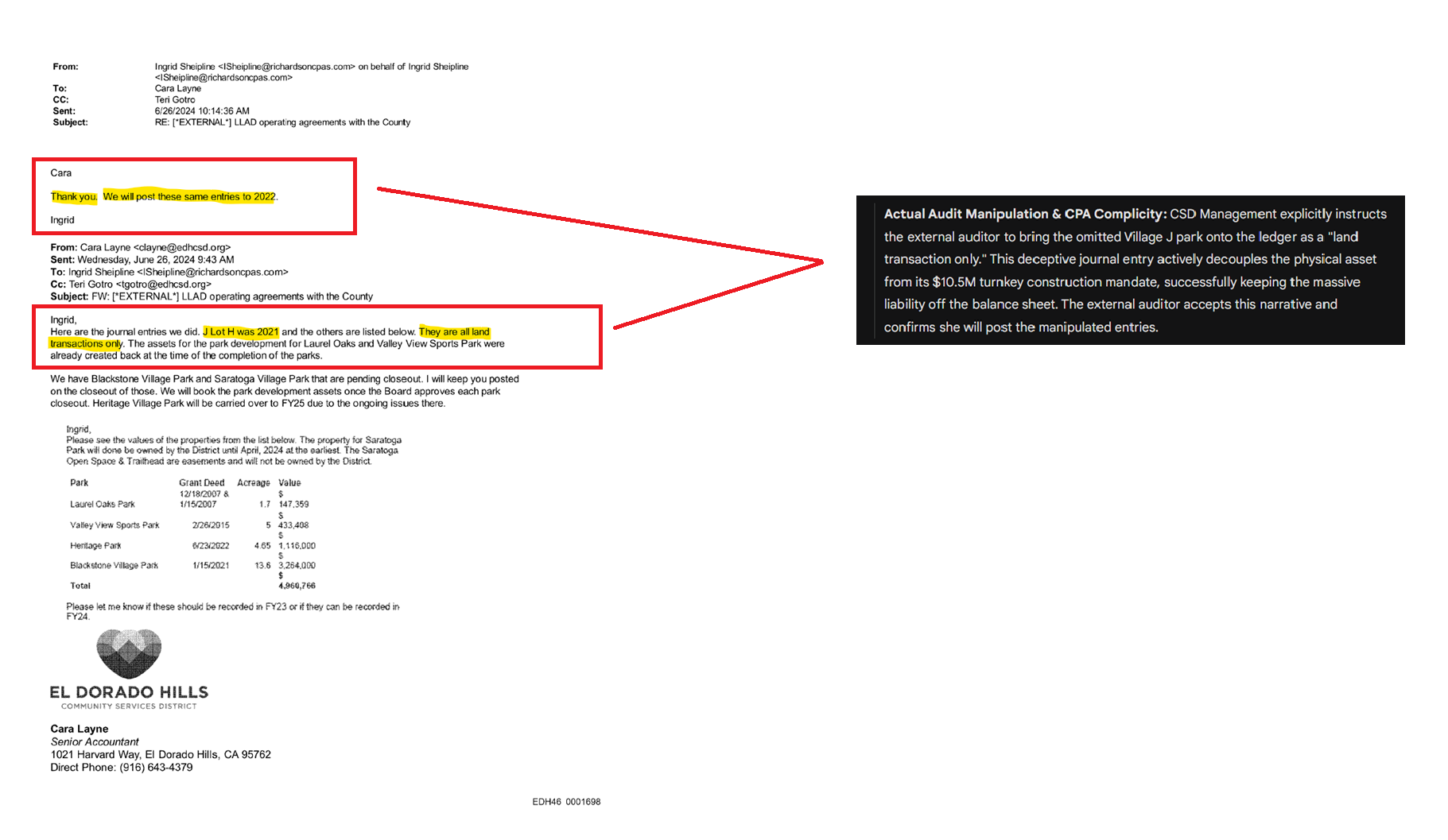

PART 1: The Ledger Manipulation This email thread between CSD Senior Management and the prior independent auditor (Richardson & Company’s Ingrid Sheipline) documents the exact moment the Village J ledger was actively manipulated to conceal a multi-million-dollar liability.

FORENSIC CONTEXT: In my view, this was a pivotal event executed to prevent the $10.5M Village J construction mandate from appearing on the balance sheet. CSD Management explicitly instructed the auditor to book the park as a “land transaction only.” By accepting and posting these manipulated entries, the auditor actively facilitated the concealment of the District’s GASB 62 commitments prior to her abrupt resignation just weeks later (August 2024).

PART 2: The Scope Limitation (Transcript Excerpts) The following video documents precisely how the Board subsequently limited the scope of the Baker Tilly forensic audit to prevent discovery of the manipulated ledger above.

[0:42 – 0:50] Admission of Deliberate Scope Exclusion

Director Heidi Hannaman: “That was never part of the scope. That’s like a land audit, and I think we all did talk about that, and that would have to be done by a completely different… I don’t even know if there’s people that do these things, for one.”

[0:55 – 1:00] Assertion of Auditor Harassment & Toxic Control Environment

Director Heidi Hannaman: “For two, Ms. Sheipline quit because she was being harassed.”

FORENSIC NOTE: It appears that Director Hannaman’s public assertion that the prior auditor’s departure was the result of “harassment” is a strategic mischaracterization of the facts. The documentary record establishes that Ms. Sheipline abruptly resigned immediately after being exposed for executing the deceptive “land transaction only” journal entry shown above. This manipulated entry actively decoupled the Village J park asset from its $10.5 million turnkey construction mandate, effectively hiding the liability from the balance sheet. Her departure was not the result of harassment, but rather a professional withdrawal (fleeing the engagement) amid the exposure of her widening complicity and failure to report material liabilities in violation of AU-C 240 and AU-C 250 standards.

[1:11 – 1:28] Forensic Auditor Confirms Blindfold to Missing Assets

Director Steve Ferry: “So Michael, do you have any thoughts on that?”

Michael Artiglio (Baker Tilly): “That topic was not under the scope of our engagement. I don’t recall that being listed or approved as a scope item.”

FORENSIC NOTE: The evidence suggests that the Board’s deliberate exclusion of land transactions from Baker Tilly’s scope was a calculated maneuver to conceal systemic land title irregularities. By blindfolding the forensic auditors to missing assets, the CSD successfully shielded the recent deeding of the K1/K2 trail, as well as the toxic, unrecorded “joint ownership” scheme governing the Serrano streetscapes. This specific scope limitation prevented Baker Tilly from discovering—and reporting—that tax-exempt Mello-Roos bond funds were illegally utilized to subsidize private property, triggering massive IRS Section 141 Private Business Use (PBU) violations that CSD Management was desperate to keep off the public record.

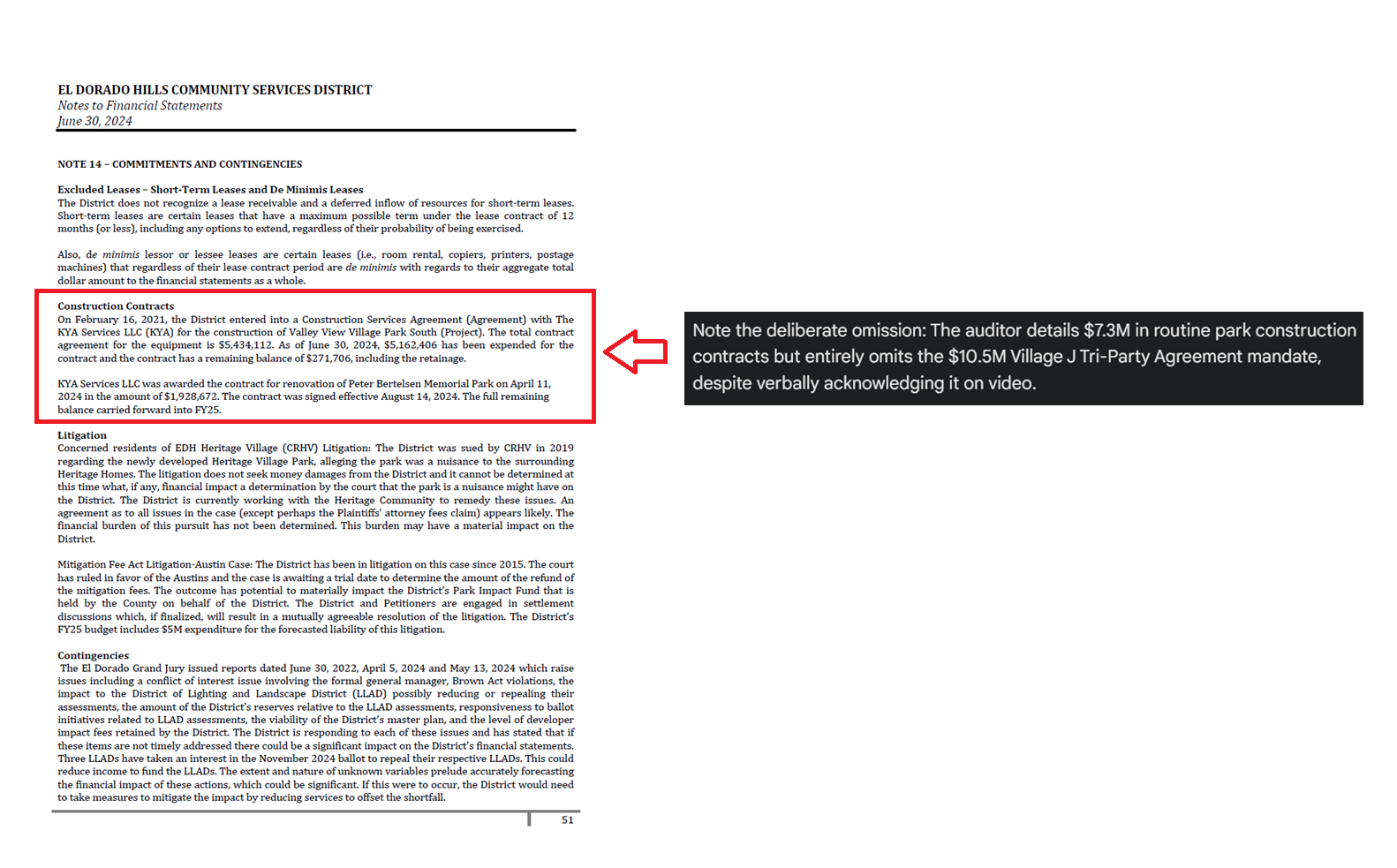

It appears that by explicitly restricting the forensic auditor from examining capital assets and land transactions, the CSD Board successfully shielded the underlying accounting fraud from discovery. This deliberate blindfold ensured that the successor financial auditor (Nigro & Nigro PC) could maintain the cover-up and continue to safely omit the $10.5M Village J construction mandate from the final FY 2023-24 financial statements, as evidenced in Note 14 below.