The following video excerpt is from the July 10, 2025, EDHCSD Board of Directors meeting. This recording is archived here to provide a clear record of the Engagement Partner’s testimony in connection with his FY 2023-24 audit report and specific questions regarding the accounting treatment of the Village J Tri-Party Agreement (signed in 2020) and the associated construction mandates.

VIDEO REFERENCE POINTS:

Subject: Accounting Recognition and Construction Obligations

Relevant Timestamp: 01:15 – 01:33

Context: Discussion regarding the nexus between CFD fund remittance and the District’s obligation to provide turnkey park construction.

Transcript Excerpt: “The only reason to recognize that revenue would be to offset… you must provide all this construction first…”

FORENSIC NOTE: > In my assessment, this video provides compelling evidence that the auditor (Paul Kaymark) possessed actual knowledge of the massive, unfunded park liability.

The Admission: He explicitly states on camera that the District “must provide all this construction,” confirming a material financial commitment that legally requires disclosure (GASB 62).

The Omission: Despite demonstrating this direct knowledge on video, Kaymark did not report the $10.5 million debt in the 2024 audit, yet still issued the District a “clean” financial rating (AU-C 240).

The Significance: In my opinion, this recording defeats any defense of an “accidental oversight.” The evidence strongly suggests the CPA willfully ignored the liability, effectively shielding it from taxpayers and regulators.

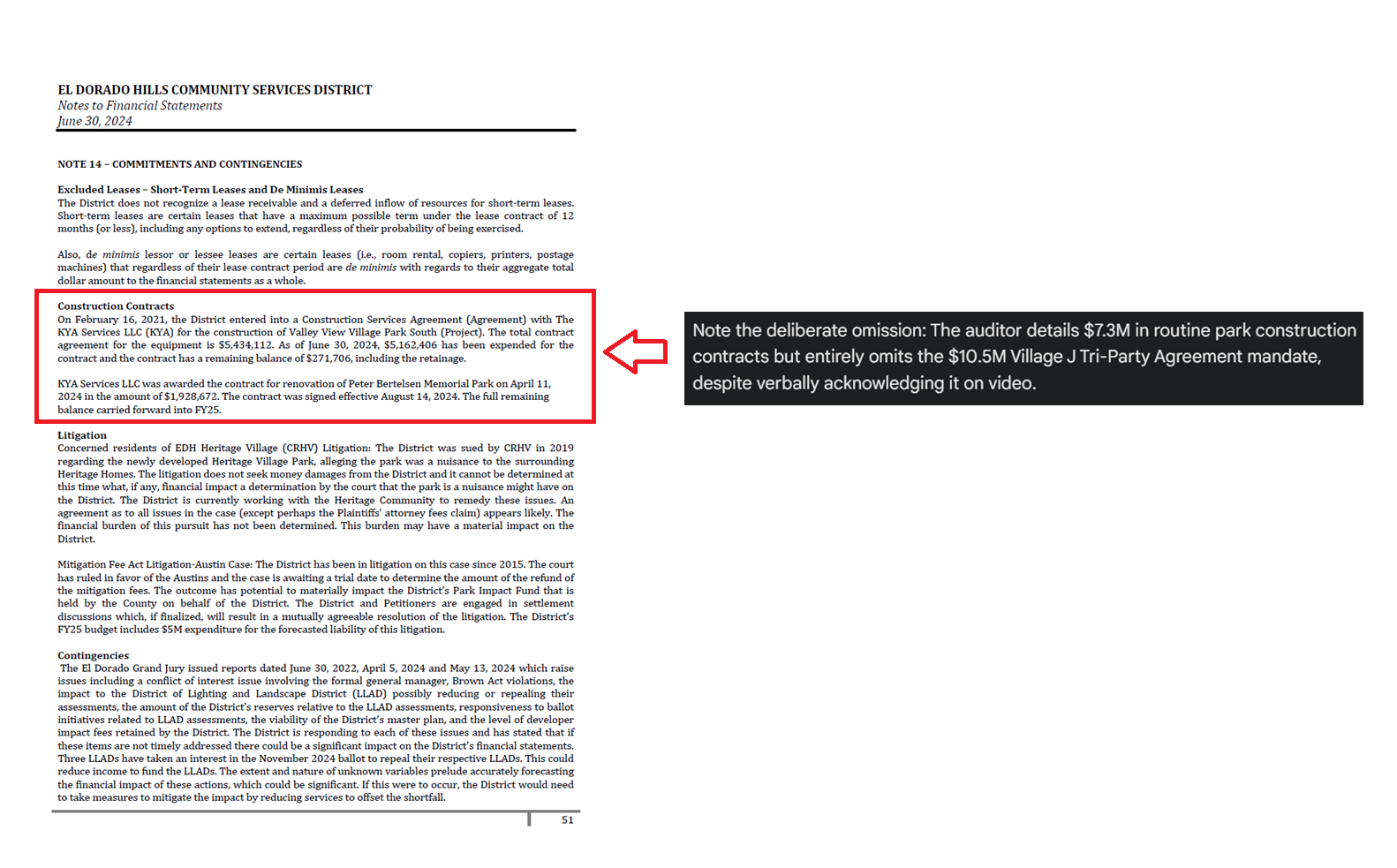

FORENSIC ASSESSMENT: > In my view, the CSD Board’s explicit decision to restrict the subsequent forensic auditor from examining capital assets and land transactions acted as a calculated shield. By artificially blinding the forensic review, the Board effectively cleared the path for the successor financial auditor (Nigro & Nigro PC) to leave the $10.5 million Village J construction mandate entirely off the final FY 2023-24 financial statements. As evidenced in Note 14 below, I believe this targeted scope limitation is the exact mechanism that allowed a massive public liability to successfully vanish from the official ledger.